Floor Plan Lending Ucc

The U C C Churches Have Been Focusing On Going Green So We Decided To Build Our Library Little Free Libraries Little Free Library Plans Free Library

What Is A Ucc Filing How A Ucc Lien Works Willcox Buyck Williams

How Can A Ucc 1 Blanket Lien Affect Your Business

Office Building Floor Plan Hingham Congregational Churchhingham Congregational Church

Ucc Financing Statement Collateral Description Fundamentals Csc

Ucc 128 Bar Code Labels What Are They How To Print These Labels Barcode Labels Shipping Labels Labels

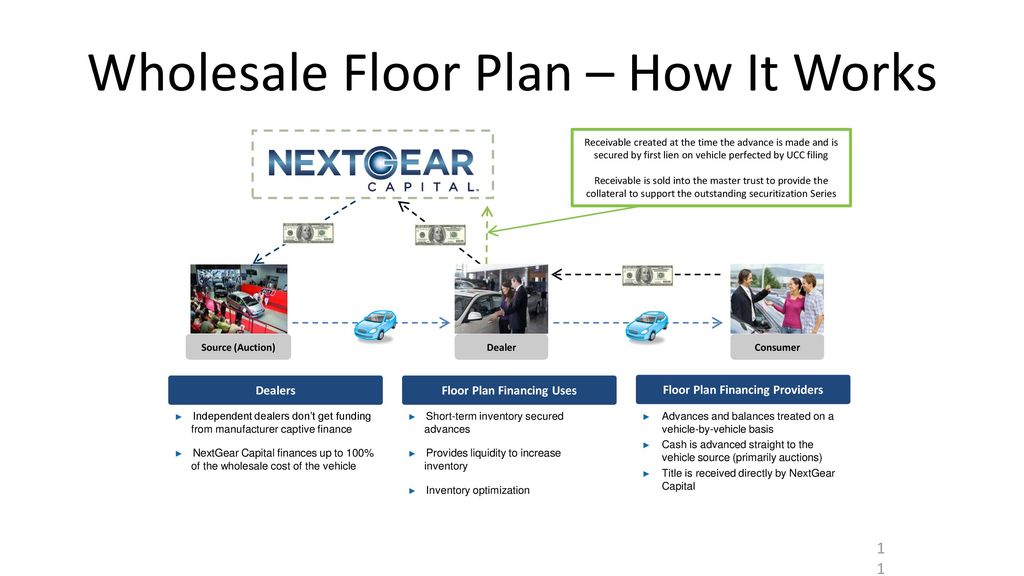

As each individual new car is shipped to the dealer it is an industry standard practice that the manufacturer drafts the.

Floor plan lending ucc. Although the lender filed a ucc 1 financing statement to perfect its lien the floor plan loan agreement also required all original vehicle title documents to be transferred to and held by the lender. For example a dealer might be able to borrow 10 million over the year to purchase 300. The nationwide industry standard process is called floor plan lending and it works like this. The loans are often made with a one year term and based on an aggregate budget.

The dispute arose because the floor plan lender refused to turn over possession of the certificate of title. Supplementing working cash with a floor plan is a tried and true method to grow business. When a certificate of title is not transferred to the buyer the court in bank one found that a buyer s purchase of a vehicle was not sufficient. Floor plan lending is a form of inventory financing for a dealer of consumer or commercial goods in which each loan advance is made against a specific piece of collateral.

Based upon what the car dealer thinks will sell the best the new car dealer places its new car orders with the manufacturer. The debtor later filed for bankruptcy and the lender continued to hold the certificates of title after subsequent sales to consumers as a means. Uniform commercial code ucc requires a bank to enter into a security agreement with the. In order to facilitate the ability of lenders to floor plan or otherwise finance the acquisition of inventory by dealers of titled equipment the ucc in almost all states provides that filing a financing statement is the proper method of perfection d uring any period in which collateral subject to a state certificate of title law is.

Floor plan financing is also done for large appliances mobile homes and boats among other items and these products are usually sold to consumers with a financing contract. Floor planning is a form of financing for large ticket items displayed on showroom floors. This booklet addresses the risks associated with floor plan lending and discusses risk management practices for floor plan lending. Find out how nextgear capital dealers are tackling the challenges of today s market head on by properly utilizing their lines of credit.

This booklet applies to the occ s supervision of national banks and federal savings associations. For example automobile dealerships utilize floor plan financing to run their businesses.

Get Low Cost Merchant Cash Advance Leads To Reap Huge Profits Lead Generation Marketing Cash Advance Lead Generation

Dealer Funding Good Afternoon I Am Susan Moritz Vice President Of Development For Nextgear Capital The Focus Of This Workshop Is Leveraging Inventory Ppt Download

Ucc Frequently Asked Questions Tennessee Secretary Of State

What Is A Ucc 1 Filing How Do Ucc Liens Work Valuepenguin

Https Www Sidley Com Media Publications Sec20 Chapter26 Usa Pdf La En

Sec Filing Neos Therapeutics Inc

Exhibit1042termloancredi

Purchase Money Security Interests Pdf Free Download

Legal Magic Turning Real Property Foreclosures Into Uniform Commercial Code Sales New Miami Blog

Banking Finance Attorneys Legal Counsel Roth Jackson Legal Services Richmond Va Mclean Va

Edgar Filing Documents For 0000920371 20 000101

Ucc Liens Attorney In New York Dedicated Debt Defense

Updated The Economic Injury Disaster Loan Eidl Program Vs The Paycheck Protection Program Ppp Comparison Chart Krost

A01creditagreementa01

Evolent Health Inc 2019 Current Report 8 K

Https Www Michigan Gov Documents Buymichiganfirst 2001367 288027 7 Pdf

Calms Compass Floorplan Wholesale Product White Clarke Group

Finance Advisory Federal Reserve Revises Main Street Lending Program Adds Third Option News Insights Alston Bird

Edgar Filing Documents For 0001437749 20 013623

Banking And Financial Services Perkins Thompson

Https Www Ohiosos Gov Globalassets Publications Busserv Uccguide Pdf

Supreme Court Decides On Applicability Of Section 1 Of The Federal Arbitration Act Page 27 Of 66 Business Law Today From Aba

Https Www Kccllc Net Whitestar Document 1912521190621000000000045

Https Www Chhsm Org Wp Content Uploads 2019 03 Mitchell Acosta Creative Use Of Space Pdf

98007 Zip Code Registered Businesses Permit Records Property Owners Uniform Commercial Code Ucc Filings Clustrmaps Com

Https Www Umpqua Edu Images Resources Services Academic Course Catalog Downloads 2020 21 2020 21 Ucc College Catalog Pdf

Creditors Rights Financial Restructuring And Bankruptcy Mcglinchey Stafford Pllc

Http Www Jtexconsumerlaw Com V14n1 V14n1 Lien Pdf

Our History Hingham Congregational Churchhingham Congregational Church

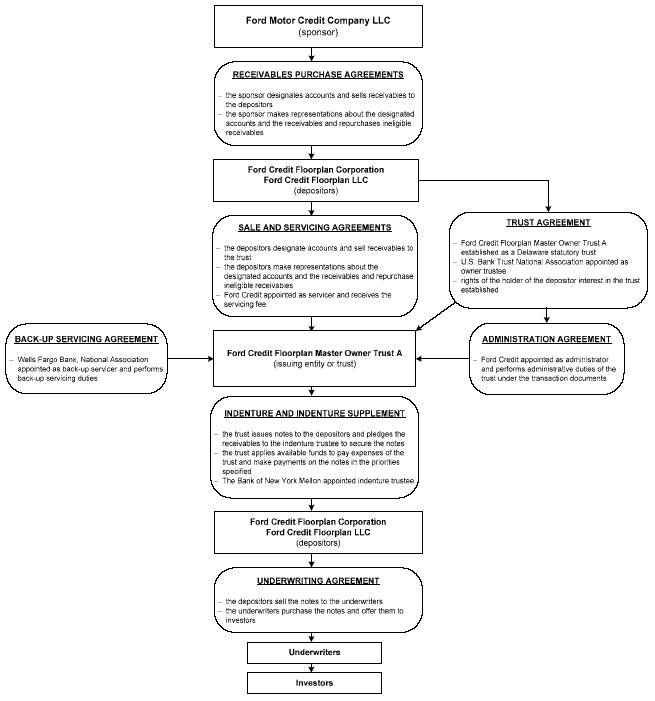

Ford Credit Floorplan Master Owner Trust A

Stories Archives United Church Of Christ Cornerstone Fund

Will They Have Horrendous Complications For Co Ops Ucc Article 9 Revisions The New York Cooperator The Co Op Condo Monthly

Announcing 20 Year Terms On Signature Pool Loans

98008 Zip Code Registered Businesses Permit Records Property Owners Uniform Commercial Code Ucc Filings Clustrmaps Com

Best Practices Debt Refinance And Preserving Purchase Money Security Interests Starfield Smith Attorneys At Law

Rapid Finance Review 2020 Business Com

Exhibit

Tcfs72 9avdoxm

Our Services Velawcity Legal Support Services

Dealer Resources Nextgear Capital

Fourth Amendment To Facility Agreement Dated As Of October 2

Between The Lines How Not To Perfect A Security Interest In A Right To Payment Under An Insurance Policy Between The Lines

The Abcs Of Pmsis A Primer On Purchase Money Security Interests Pmsis Part 1 Lexology