Floor Plan Financing Bonus Depreciation

Kbkg Tax Insight Impact Of Bonus Depreciation For Companies With Floor Plan Financing Kbkg

2019 Bonus Depreciation Update For Auto Dealers Councilor Buchanan Mitchell Cbm

Bonus Depreciation Rules Favor Dealerships With Floor Plan Financing Interest 2019 Articles Resources Cla Cliftonlarsonallen

Product Page Skyline Homes Floor Plans Manufactured Homes Floor Plans Modular Home Plans

Thank You Factory Tour The Home Store Modular Home Floor Plans Two Story House Plans Pole Barn House Plans

2 Storey House Plans Floor Plan With Perspective New Nor Cape House Plans House Plans 2 Storey House Layout Plans

The tcja also disallows bonus depreciation if the floor plan financing interest exception applies.

Floor plan financing bonus depreciation. The tax cuts and jobs act of 2017 tcja increases the bonus depreciation rate from 40 to 100 for property acquired after sept. Floor plan financing and bonus depreciation exception. Fortunately the recent proposed regulations clarified three key elements of the interaction between the interest expense and bonus depreciation rules. Tax strategies bonus depreciation rules favor dealerships with floor plan financing interest.

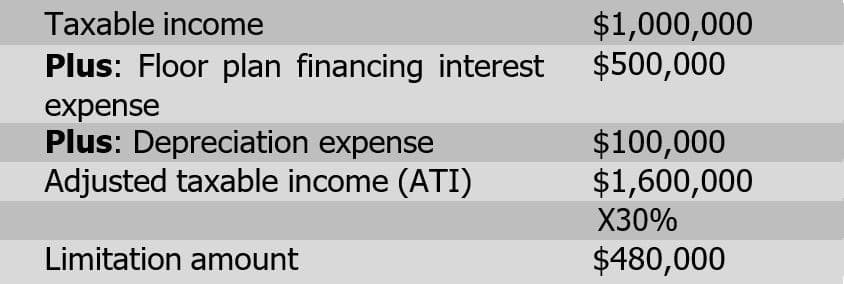

Floor plan interest remains fully deductible but interest expense on debt other than floor plan financing debt may be limited due to 1 and 2. Floor plan financing interest expense remained fully deductible under tax reform. The proposed regulations provide for a special rule applicable to taxpayer with floor plan interest determining when it is taken into account for purposes of the 163 j business interest limitations. Dealerships that take the floor plan financing interest exclusion in computing their limit can t claim 100 bonus depreciation for their fixed asset additions.

10 30 2019 under the tax reform rules passed in 2017 the deduction for net business interest expense was generally limited to 30 of a dealership s adjusted taxable income plus 100 of floor plan financing interest expense. The automobile dealership operating company benefits from floor plan financing so bonus depreciation will not apply to assets placed into service by the company in 2019. Generally taxpayers in those industries cannot take bonus depreciation on their assets as a result of special rules in sec. This planning opportunity paired.

Taxpayers that have assets used in regulated utilities or that have had floor plan financing interest also received specific guidance in the 2019 proposed regulations. 27 2017 and placed into service after dec. This leads to an unexpected trade off. Specifically the 2019 proposed regulations address the following.

Through some tax planning the automobile dealership decides the new construction location will be owned by a new real estate holding company. Auto dealers with floor plan financing interest are still eligible for bonus depreciation. But it came at a cost. As long as the dealership does not need to use the floor plan interest exception to fully deduct business interest including floor plan interest then the dealership is still eligible to take advantage of the favorable full expensing provisions of.

If such interest was initially considered floor plan financing interest then most auto dealers would be prohibited from taking the accelerated deductions for 100 bonus depreciation.

The Taylor House Plans First Floor Plan Ideas For Kitchen Into Great Room Floor Plans House Plans Garage Plans Detached

Plan 89988ah 3 Bed Craftsman Ranch With Open Concept Floor Plan Floor Plans Ranch Open Concept Floor Plans Ranch House Plans

Cypress Iii Floor Plan Bluestone Eastwood Homes Floor Plans How To Plan Richmond Homes

Plan 33117zr Net Zero Energy Saver House Plan Mediterranean House Plans House Plans Ranch House Plans

Plan 17801lv Stunning Open Floor Plan New House Plans Best House Plans Open Floor Plan

The Mcmillan Floor Plan Signature Collection Basement Floor Plans Rambler House Plans Basement House Plans

3 Bedroom Floor Plan C 9810 Hawks Homes Manufactured Modular Conway Little Rock Arkansas Bedroom Floor Plans Floor Plans 3 Bedroom Floor Plan

Ranch Style House Plan 3 Beds 2 Baths 1796 Sq Ft Plan 70 1243 Ranch Style House Plans Best House Plans Ranch House Plans

Plan 765011twn 5 Bed Beach Y House Plan With Two Upstairs Options Included House Plans Pier And Beam Foundation Architectural Design House Plans

Highland Homes Shennandoah Ii Floor Plans Highland Homes How To Plan

Plan 69554am 3 Bedroom Craftsman Ranch Home Plan Floor Plans Ranch Craftsman Ranch Craftsman House Plans

Laundry Craft Room Floor Plans Google Search Garage House Plans Bedroom Floor Plans Garage Floor Plans

Details Template Mobile Home Floor Plans Triple Wide Mobile Homes Modular Home Plans

Plan 022h 0022 House Plans Traditional House Plan Floor Plans

Plan 69270am European Luxury Plan With Angled Garage Garage Floor Plans Garage House Plans Country Style House Plans

Floorplan The Breeze Ii 34ssp28764ah Clayton Homes Of Athens Athens Tn House Floor Plans Clayton Homes Mobile Home Floor Plans

Lynnwood Gif 450 294 Floor Plans Ranch Raised Ranch Remodel Ranch House Plans

Country Style House Plan 2 Beds 2 Baths 1350 Sq Ft Plan 30 194 Country Style House Plans Floor Plan Sketch Floor Plan Design

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcqkeyoweol9qj1 Srfysmpcbicshchjhdme Mbk79qmjzva8jab Usqp Cau

Find Your Perfect Floor Plan Floor Plans Manufactured Homes Floor Plans House Floor Plans

The Keys Collection Hemingway Floor Plan In Solivita Kissimmee Fl Entry Foyer Kissimmee Fl Kissimmee

Residence 1 New Home Plan In Rancho Bella Vista Paloma One Storey House Floor Plans Dream House Plans

Cottage Style House Plan 75237 With 3 Bed 2 Bath 3 Car Garage Ranch Style House Plans Ranch House Plans Best House Plans

San Benito Floorplan 1848 Sq Ft Heritage Ranch Floor Plans Heritage House Plans

Southampton I 7023 6 Bedrooms And 6 Baths The House Designers New House Plans Ranch House Plans House Plans

Whitmore Floor Plan At Camburn In Clover Sc Taylor Morrison Floor Plans New Homes How To Plan

Plan 23777jd 5 Bed Modern House Plan With Bonus Room And Second Level Master In 2020 Modern House Plan House Plans Modern House Plans

Portico Floor Plan Building A Porch House Plans Porch Design

Chloe Ii Floor Plan At Kingsley Creek In Fernandina Beach Fl Taylor Morrison Fernandina Beach Screened In Patio Floor Plans

Plan 83866jw Giant Open Floor Plan Acadian House Plans Barn House Plans House Plans

Plan 22458dr Tiny Weekend Getaway House Plan With Options House Plan With Loft House Plans Tiny Houses Plans With Loft

West Ridge Triple Wide Floor Plans Mobile Home Floor Plans Floor Plans House Floor Plans

Small Cabin Floor Plan Love This One But It Doesn T Really Need Two Bathrooms Description From Pinterest Guest House Plans Tiny House Plans Cabin Floor Plans

Country Craftsman Farmhouse House Plan 82085 Farmhouse Style House Plans Craftsman Style House Plans Craftsman Farmhouse

Durango Homes Duplex Series U Dpx 3270a Cavco Duplex Floor Plans Manufactured Homes Floor Plans Mobile Home Floor Plans

2015 Thor Challenger 37tb Rv Floor Plans Floor Plans Camper Flooring

European Style House Plan 5 Beds 3 Baths 2349 Sq Ft Plan 36 442 5 Bedroom House Plans House Floor Plans Bedroom House Plans

Floorplan 3536 76x28 Ck4 2 Jamestown Mod 58jat28764jm Clayton Homes Of Statesville Statesville Nc Floor Plans Modular Floor Plans Modular Homes For Sale

Plan 61144 Log Home Plans Log Home Floor Plans Garage House Plans

Grand Manor Triplewide Clawson Mobile Home Floor Plans Modular Home Floor Plans Manufactured Homes Floor Plans

Quinlan V2 Barndominium Floor Plan In 2020 Barndominium Floor Plans Barndominium Garage House Plans

Floorplan Image Of Keystone Alpine Model 3900re 3901re Rv Floor Plans Grand Design Rv Trailer Living